Basic Accounting Concept – The Matching Principle

The matching concept is one of the most crucial concepts of accrual basis in accounting. It demands that one should recognize incomes as well as any related costs together within the same reporting period. Implementing this concept can be complicated for some small firms. Hence, they should engage an accounting firm in Johor Bahru to help them with these tasks.

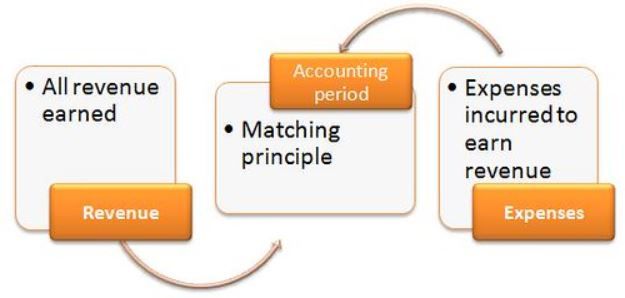

Under the matching principle, you should record the revenue and certain expenses simultaneously using double entry accounting if there is a cause-and-effect relationship, thus. If such a relationship is absent, you have to charge the cost to expense instantly. The matching principle requires people to document the full impact of a transaction in the same reporting period.

Some instances of the matching concept include:

Commission

A salesperson gets a 3% commission on the sales he transported and recorded in March. His employer pays him the commission of RM3,000 in April. His employer needs to document the commission expense in March when preparing the trial balance.

Depreciation

A business purchases a machine for RM240,000, and they expect to use it for eight years. It needs to charge the expense of the machine to depreciation expenditure (Also see Impairment versus Depreciation of Fixed Assets) at the price of RM30,000 annually for eight years.

Staff member bonuses

Under a bonus plan, a staff member earns a bonus amounting to RM20,000 based on her performance throughout the year. Although you are going to pay him the bonuses in the next year, you should document the bonus expense in the year when the staff member gained it. This share the common concept for doing accrued revenue.

Wages

The pay period for hourly basis workers finishes on July 28. However, the workers keep earning wages until July 31, and they receive the amount on August 3. Thus, the employer ought to document the expenditure in July for those salaries they earn from July 28 to July 31.

As the use the matching principle may need a large workforce, the controllers of the company usually do not utilize it for unnecessary items. For instance, creating a journal entry which spreads the recognition of a vendor invoice of RM150 over three months may not be logical, even if the fundamental impact will affect all three months. Rather, you will charge such tiny things to expense as incurred.

If you are not implementing the matching principle, you will use the cash method of accounting. By using this method, you will only record profits when you obtain cash or when you pay for expenditures.